Dubai Insurance Guide for Expats and Residents (2026)

Dubai has a growing insurance market with dozens of providers, government mandates, and plan tiers that look similar but cost very differently. If you just moved here, the options can feel like a maze.

The good news is this: the right plan for you comes down to your life situation, not just your budget. A single expat working a corporate job needs a completely different setup than a family of four running a business in a free zone. Insurance in Dubai is not optional in many cases. Health insurance is mandatory. Car insurance is required if you drive. Business insurance becomes important as you grow. The problem is not availability. The problem is choosing the right plan without overpaying or missing something important. Most people either buy the cheapest plan or over-insure without knowing why.

This guide breaks it down based on your situation so you can make a clear decision.

If You Are a New Expat in Dubai

The first 30 to 90 days in Dubai move fast. Between visa processing, finding an apartment, and opening a bank account, insurance often gets pushed to the bottom of the list. That is a mistake worth avoiding.

What you need immediately:

Basic health insurance: Mandatory by law. If your employer does not provide it, you need to get it before your residency visa is stamped.

Emergency coverage: Make sure your plan covers emergency room visits and hospitalization from day one. Some basic plans exclude this for a waiting period.

Repatriation coverage: This pays to transport you back to your home country in a medical emergency. It is easy to skip, and painful not to have.

What you can wait on:

Life insurance (unless you have dependents)

Critical illness add-ons

Income protection policies

What people usually get wrong:

Choosing the cheapest plan with very limited coverage

Ignoring waiting periods for certain treatments

Not checking if their preferred clinic is covered

If You Have a Family

Bringing family to Dubai means more moving parts. A spouse and children each need their own insurance tied to your residency sponsorship. The cost adds up, but so do the coverage gaps if you choose poorly.

Key coverage areas for families:

Maternity coverage: Many basic plans offer limited maternity benefits or exclude them entirely. If you are planning to have children in Dubai, a maternity coverage plan is essential. Check the waiting period, which is usually 12 months from enrollment.

Pediatric dental and vision: Not always included in standard family plans. Worth adding if your children are school-age.

School and vaccination records: Dubai schools ask for updated vaccination records. Some insurers offer pediatric wellness packages that make this straightforward.

Family plan vs. individual plans:

In Dubai, you can insure each family member on your corporate plan (if the employer allows) or purchase a separate family plan. For families with three or more members, a group family plan is usually more cost-effective. Compare the annual premium against the combined cost of individual plans before deciding.

Domestic help coverage:

If you employ a nanny or housekeeper in Dubai, you are legally required to provide them with health insurance. Some family plans allow adding domestic workers at a discounted rate. This is easy to overlook and carries a legal penalty if missed.

Better decision:

Choose a mid-tier plan instead of the cheapest.

Add coverage based on actual family needs

If You Own a Car

Car insurance in Dubai is mandatory by law. You cannot register or renew a vehicle without it. But there is a significant difference between the minimum required coverage and what actually makes sense for daily driving in Dubai.

Two main options:

Third-party liability.

Comprehensive insurance.

What you should do:

Choose comprehensive if your car is new or valuable.

Use a third-party only for older vehicles.

Common mistakes:

Going for the cheapest policy without roadside assistance.

Not checking the claim process or insurer reputation.

If You Run a Business

Business owners in Dubai have more mandatory insurance requirements than individual residents. Whether you operate a mainland company or a free zone entity, getting insurance right protects both your team and your finances.

What the law requires:

Employee health insurance: Mandatory for all staff under the Dubai Health Authority (DHA) framework. You must provide coverage that meets the Essential Benefits Plan (EBP) standard at a minimum.

Workers' compensation: Required by UAE labor law if an employee is injured while on duty.

Professional indemnity insurance: Required for certain business types such as legal firms, healthcare providers, and financial advisors. Check with your licensing authority.

Smart coverage to add:

Group life insurance: Common in competitive industries to attract talent. Not mandatory but increasingly expected by mid-level professionals.

Business interruption insurance: Covers lost revenue if your business is temporarily forced to close due to an insured event, such as a fire.

Cyber liability insurance: Growing in importance as more Dubai SMEs move to digital operations and cloud storage.

Key person insurance: If your business depends heavily on one or two individuals, this protects the company if they become unable to work.

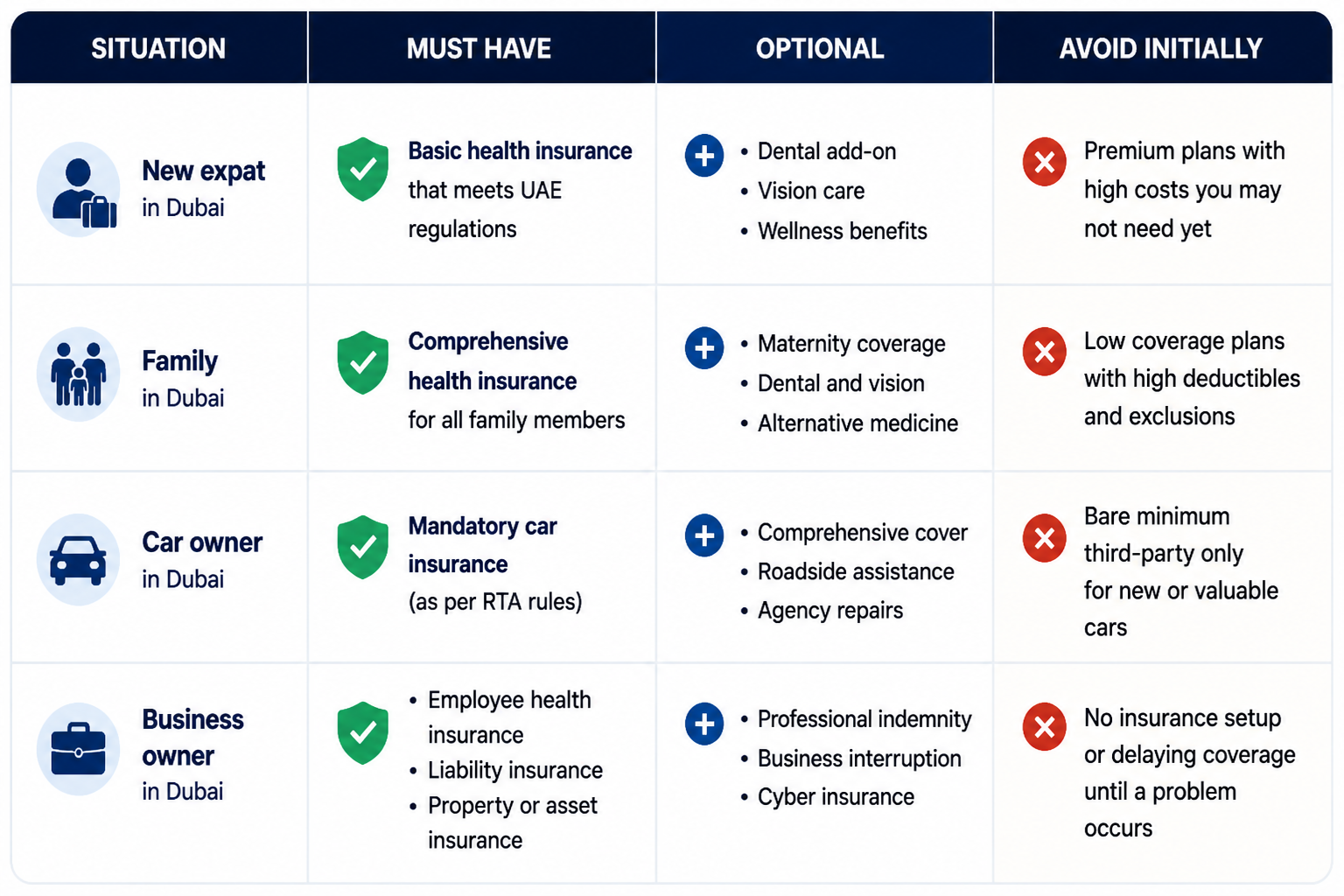

Here’s a simple breakdown of what insurance you actually need in Dubai based on your situation.

Situation | Must Have | Optional | Avoid Initially |

New expat | Basic health insurance | Dental add-on | Premium plans |

Family | Comprehensive health plan | Vision, dental | Low coverage plans |

Car owner | Mandatory car insurance | Roadside assistance | Bare minimum policy |

Business owner | Liability + employee insurance | Asset protection | No insurance setup |

Use this table to avoid overpaying and focus only on the coverage that fits your lifestyle, family needs, or business setup.

Dubai rewards people who plan ahead. Insurance is no different. You do not need the most expensive plan on the market. You need the right one for where you are right now. Start with the basics, stay compliant, and revisit your coverage every time something in your life changes. That one habit will save you more money and stress than any single policy ever could.

What is the minimum health insurance required in Dubai?

A basic plan that meets DHA requirements is mandatory. It usually covers essential treatments and emergency care.

Is third-party car insurance enough in Dubai?

It is enough legally, but not practical for new or expensive cars. Comprehensive insurance offers better protection.

Do businesses in Dubai need insurance?

It is not always mandatory, but liability and employee insurance are strongly recommended.

How much does health insurance cost in Dubai?

Basic plans can start low, while comprehensive plans cost more depending on coverage and provider.

Should expats upgrade insurance plans later?

Yes. Many expats start with the basics and upgrade once they understand their needs.

Related Posts

Insurance for Freelancers in Dubai: Complete Guide

Freelance or self-employed in Dubai? Learn how health, liability, indemnity, and income protection insurance work for expats.

What Happens When Missed Health Insurance Renewal in Dubai?

Missed your health insurance renewal in Dubai? Learn about fines, visa issues, medical bills, grace periods, and what to do next.