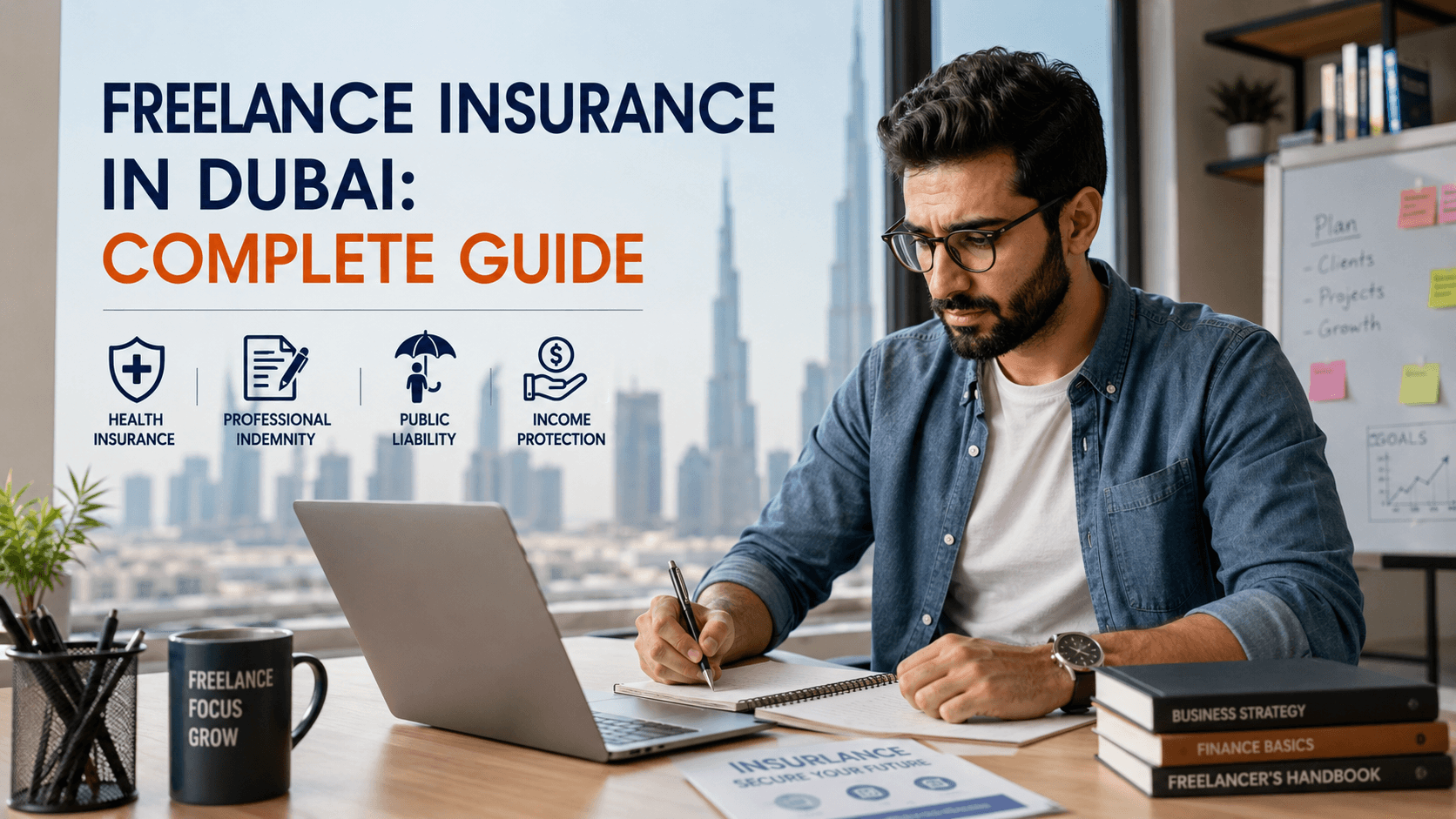

Insurance for Freelancers in Dubai: Complete Guide

Dubai is full of freelancers now. Designers, consultants, developers, coaches, creators, writers, marketers, photographers, and remote workers are building careers without a fixed employer. That freedom is great, but insurance becomes your responsibility.

When you work for a company, HR usually handles your health insurance. When you work for yourself, you need to understand what cover is required, what cover is optional, and what can protect you if a client, patient, venue, or third party makes a claim against you.

Understanding the Dubai Insurance Landscape for Freelancers

Health insurance is mandatory for Dubai residents. Employers in Dubai are responsible for providing health insurance for their employees, while sponsors must extend coverage to dependents, including spouses, children, and domestic workers. For freelancers and self-employed expats, the main question is: who sponsors your visa?

If you are self-sponsored, on a freelance visa, or living in Dubai under a remote work visa, you will usually need to arrange your own health insurance. The UAE’s official virtual work visa page also lists health insurance as a required document for remote workers applying to live in the UAE while working for an overseas employer.

Corporate plans are usually arranged by employers and may include group pricing, HR support, and easier renewals. Individual plans are purchased directly by the resident, freelancer, sponsor, or business owner. They give you more control, but you need to compare the details yourself.

What If You Are an Expat Freelancer in Dubai?

If you are an expat freelancer in Dubai, your insurance is part of your residency setup. Having overseas clients, foreign income, or an international contract does not automatically mean you are covered in the UAE. Your policy should be valid for treatment in the UAE and suitable for your visa type. This matters for:

Freelance visa holders

Remote workers

Self-sponsored consultants

Spouse-sponsored freelancers

Business owners

Dependents under your sponsorship

Dubai’s remote work program states that health insurance must be valid in the UAE for at least one year, and travel insurance may be accepted only if it includes the required coverage.

Types of Insurance Essential for Freelancers and Self-Employed Workers

Insurance Type | What It Covers | Who Should Consider It |

Health insurance | Medical treatment, hospital care, and outpatient care | All Dubai residents |

Professional indemnity | Claims linked to advice, errors, or negligence | Consultants, marketers, designers, IT experts |

Public liability | Third-party injury or property damage | Trainers, photographers, event workers, visiting consultants |

Income protection | Loss of earnings due to illness or injury | Freelancers with no paid sick leave |

Health Insurance

Health insurance is the first cover every freelancer should sort out. A basic plan may help with residency requirements, but it may not be enough if you use clinics often. Look beyond the price and check what you actually get.

Review:

Inpatient hospital cover

Outpatient doctor visits

Specialist consultations

Emergency treatment

Medicine cover

Critical illness benefits

Maternity benefits

Pre-existing condition rules

Co-payment amounts

Annual claim limits

A freelancer with regular medication or family medical needs should not choose insurance based only on the cheapest quote.

Professional Indemnity Insurance

Professional indemnity insurance protects you if a client claims your service, advice, work, or mistake caused financial loss. This matters if you provide professional services, such as:

Marketing strategy

Website development

Business consulting

Accounting support

Design work

IT services

Training or coaching

Example: a freelance consultant provides operational advice to a client. The client follows it, loses money, and blames the consultant. Professional indemnity cover can help with legal defence and settlement costs, depending on the policy.

Public Liability Insurance

Public liability insurance helps if your work causes injury or property damage to someone else. This is useful for freelancers who meet clients, work at events, visit offices, or handle equipment.

Example: a freelance photographer damages expensive venue equipment during a shoot. Or a personal trainer’s client gets injured during a session and files a complaint. Public liability cover can protect against these kinds of third-party claims.

Income Protection Insurance

Freelancers do not usually get paid sick leave. If you cannot work because of illness or injury, your income may stop immediately. Income protection insurance can help replace part of your earnings for a period, depending on the policy. This is especially useful if you:

Depend fully on freelance income

Have monthly rent or loan payments

Support family members

Work in a physical profession

Have no emergency savings

Why Health Insurance Alone Is Not Enough

Health insurance protects your body. It does not protect your freelance business. That is the mistake many independent professionals make. A web developer can be blamed for a site crash. A marketing freelancer can be blamed for the loss of ad budget. A business consultant can be blamed for poor advice. A photographer can damage property during a shoot. A trainer can face an injury claim.

Health insurance usually does not cover those business risks. That is where professional indemnity and public liability insurance become useful.

How to Choose the Right Insurance Plan

Start with your real risk, not the cheapest quote. Ask yourself:

What type of work do I do?

Can my advice cause financial loss?

Do I visit client locations?

Do clients visit my workspace?

Do I use equipment around others?

Do I sponsor dependents?

Do I need maternity cover?

How often do I visit doctors?

What monthly premium can I sustain?

Then compare policies side by side. Check the exclusions, waiting periods, claim process, cancellation rules, co-payments, deductibles, and renewal terms. If you are unsure, speak to a licensed insurance broker instead of guessing.

Legal and Regulatory Framework

Dubai’s health insurance system is regulated under Dubai Health Law No. 11 of 2013. The law makes health insurance mandatory in Dubai and places responsibility on employers for employees and sponsors for dependents. The official Dubai portal states that sponsors must extend health insurance coverage to dependents, including spouses, children, and domestic workers. For remote workers, valid health insurance is part of the UAE virtual work visa application documents.

Do freelancers in Dubai need health insurance?

Yes. Dubai residents need valid health insurance. Freelancers usually arrange their own policy unless they are covered by an employer, spouse, or sponsor.

Can I use international insurance for a Dubai freelance or remote work visa?

Sometimes, but it must be valid for UAE treatment and accepted for the visa process. Dubai’s remote work programme says health insurance must be valid for the UAE.

Who pays for health insurance if I am self-employed?

Usually, you do. If you are self-sponsored or working independently, insurance becomes part of your personal or business costs.

Do I need insurance for my spouse and children?

Yes, if they are under your sponsorship. Dubai sponsors are required to extend health insurance coverage to dependents.

Is cheap health insurance enough for freelancers?

It may meet basic requirements, but it can have limited networks, higher co-payments, and weak outpatient cover. Check the policy before buying.

Conclusion

Freelancing in Dubai gives you control, but it also gives you responsibility. Health insurance protects your residency and medical access. Professional indemnity protects your work. Public liability protects you from third-party claims. Income protection helps if illness or injury stops your earnings. The right insurance setup depends on your visa, profession, dependents, income, and risk level.

Next Steps

Check your visa sponsorship status, review your current health insurance, confirm dependent coverage, compare business protection policies, and speak to an insurance expert for a personalized quote before your next renewal.

Related Posts

What Happens When Missed Health Insurance Renewal in Dubai?

Missed your health insurance renewal in Dubai? Learn about fines, visa issues, medical bills, grace periods, and what to do next.

Why Dubai Clinics Reject Valid Health Insurance Cards

Tired of unexpected medical billing issues? Discover why Dubai clinics reject insurance cards and learn how to secure a seamless healthcare experience today.