Hidden Cost of Cheap Insurance in Dubai (2026)

A Dubai resident visits a private hospital for what appears to be a routine procedure. The claim gets filed. Two weeks later, the insurance company rejects it. The reason? The procedure was listed as elective under their policies fine print, even though the doctor marked it as necessary. The hospital bill is AED 14,000. Out of pocket. Full amount. This is not a rare story. It plays out every week in Dubai, with residents choosing a health plan based on one thing: the lowest available premium.

Cheap insurance in Dubai is everywhere. The monthly cost is low, the signup process is fast, and it feels like you have solved the problem. But the real cost often appears later. What it does not come with is a clear explanation of what it will not cover when you actually need it. This guide is about that gap. The one between what you think you are buying and what you are actually getting.

The Biggest Problem With Cheap Insurance

The biggest problem with cheap insurance in Dubai is simple: the price is clear, but the limits are hidden. A cheap plan may look fine on paper, but it can come with:

Limited hospital or clinic network: You may not be able to visit your preferred doctor or nearby hospital without paying extra.

High deductibles and co-payments: You pay less for the policy, but more from your own pocket during treatment.

Low annual claim limits: The insurer may stop covering costs once your yearly limit is used.

Long waiting periods: Some treatments may not be covered until you have been on the plan for a few months.

Weak outpatient coverage: Regular doctor visits, tests, and medications may be poorly covered.

Slow claim approvals: You may wait longer for treatment approval or reimbursement.

Exclusions for common treatments: Some treatments you expect to be covered may not be included in the policy.

The issue is not always that cheap insurance is bad. The issue is that many people buy it without reading what is missing.

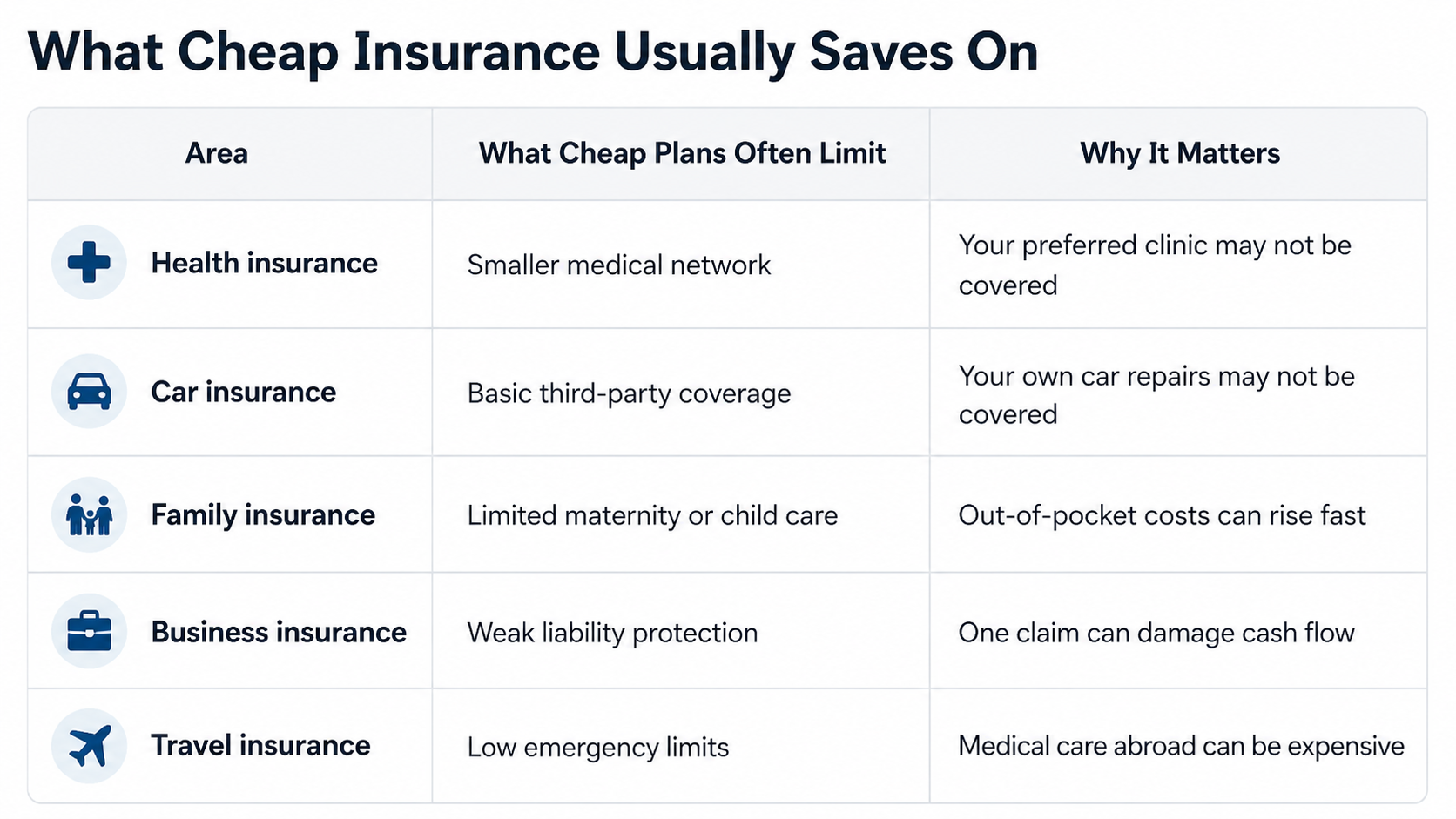

What Cheap Insurance Usually Saves On

Cheap insurance may lower your monthly premium, but it often reduces the coverage you actually need.

Area | What Cheap Plans Often Limit | Why It Matters |

Health insurance | Smaller medical network | Your preferred clinic may not be covered |

Car insurance | Basic third-party coverage | Your own car repairs may not be covered |

Family insurance | Limited maternity or child care | Out-of-pocket costs can rise fast |

Business insurance | Weak liability protection | One claim can damage cash flow |

Travel insurance | Low emergency limits | Medical care abroad can be expensive |

Check these limits before choosing a low-cost plan, because the wrong policy can lead to higher out-of-pocket costs later.

Real Life Scenarios

These are based on common situations reported across Dubai expat communities, forums, and insurance complaint boards.

Scenario 1: The maternity surprise

A couple moved to Dubai and enrolled in a basic health plan through a comparison site. The monthly premium was low and the plan looked complete on the summary page. Eight months later, they discovered the maternity benefit had a 12-month waiting period and a AED 5,000 sub-limit. Their delivery costs came to AED 22,000. The insurance covered AED 5,000. They paid the rest themselves.

Scenario 2: The specialist visit that costs double

A resident needed to see a cardiologist after a routine checkup flagged a concern. His cheap plan only covered general practitioners at government clinics. Specialist visits at private hospitals were not included. He paid AED 600 per visit out of pocket for four consultations before his employer upgraded the plan at renewal.

Scenario 3: The car accident that barely paid out

A Dubai resident with third-party only car insurance was involved in a collision that was partially her fault. The third party covered the other vehicle. Her own car sustained AED 12,000 in damage. Her policy covered nothing for her vehicle. She had chosen the cheapest motor insurance available to pass the registration check.

Scenario 4: The rejected claim

A business owner insured his five employees under a budget group health plan. One employee needed surgery. The insurer reviewed the claim and classified the procedure as elective based on its internal coding, despite the treating doctor's documentation. The claim was denied. The employee paid AED 18,000. The business owner covered half of it to avoid losing the employee.

These are not worst-case stories. They are common outcomes of prioritizing the lowest price over actual coverage.

Why People Still Choose Cheap Plans

Most people do not choose cheap insurance because they are careless. They choose it because the buying process is confusing. Here are the common reasons:

They only compare the monthly price

They trust the first quote they receive

They do not understand policy exclusions

They assume all plans are similar

They want a quick visa or a car renewal approval

They do not expect to make claims

They avoid reading long policy documents

Cheap insurance in Dubai feels like a smart saving at first. But if the plan does not match your real life, the saving is only temporary.

The Smart Way to Choose Insurance in Dubai

The goal is not to spend more. The goal is to spend correctly. Here is a straightforward way to evaluate any insurance plan in Dubai before you commit:

Step 1: Read the Summary of Benefits, not just the brochure

Every insurer in Dubai is required to provide a Summary of Benefits document. This is where the real limits are listed. Look specifically for:

Annual limits per category (not just the headline number)

Co-payment percentages

List of exclusions

Waiting period conditions

Network hospital and clinic list

Step 2: Match the plan to your actual life

Ask yourself what you are most likely to need in the next 12 months. If you are planning a family, maternity coverage matters more than dental. If you drive daily on Dubai highways, comprehensive car insurance with agency repair is worth the premium difference.

Step 3: Compare using an aggregator, but filter by coverage, not price

Insurance aggregators in Dubai have improved significantly in 2026. Platforms that let you compare plans side by side on coverage terms, not just price, give you a much clearer picture of real value. Use the filtering tools to narrow by network size, co-payment rate, and key benefits before looking at price.

Step 4: Check the insurer's claim settlement record

A plan is only as good as the insurer's willingness to pay. Look for claim settlement ratio data, which some platforms now display openly. An insurer with a 95 percent settlement rate is meaningfully different from one at 78 percent.

Step 5: Review annually

Your insurance needs in year one in Dubai are different from year three. Review your plan at each renewal. Life changes, such as a new job, a baby, a new car, or new employees, should trigger a coverage review.

The role of insurance aggregators

Using a comparison platform is the smartest starting move when shopping for insurance in Dubai. The best aggregators in 2026 do more than list prices. They show you plan-level details, filter by benefit type, and sometimes connect you directly with advisors who can explain the differences between similar-looking plans.

The key is to use the platform as a research tool, not just a price checker. Sort by coverage quality first. Then look at the price. That one change in approach is often the difference between a plan that works and one that fails you when it matters most.

Conclusion:

Cheap insurance in Dubai is not always the wrong choice. It can work if your needs are simple and you understand the limits. But if you have a family, drive a valuable car, run a business, or use healthcare often, the cheapest plan can end up costing more in the long run. The smarter move is to compare plans through an aggregator, check the exclusions, and choose coverage that fits your real situation.

Is cheap insurance in Dubai always a bad choice?

No. Cheap insurance is not always bad, but it becomes risky when the low price comes with weak coverage, high deductibles, limited networks, or slow claim support.

What is the biggest hidden cost of cheap insurance?

The highest hidden cost is paying out of pocket later. A low premium may look attractive, but you may face higher co-payments, limited hospital access, rejected claims, or repair costs that are not fully covered.

Why do cheap health insurance plans have limited hospital networks?

Cheap health insurance plans usually work with a smaller list of clinics, hospitals, and pharmacies to keep the premium low. This can become a problem if your preferred doctor, nearby clinic, or specialist is outside the approved network.

Does cheap car insurance cover my own car damage?

Not always. Third-party car insurance usually covers damage caused to others, not damage to your own vehicle. Comprehensive car insurance gives wider protection, including damage to your own car, depending on the policy terms.

What should I check before buying cheap insurance in Dubai?

Check the claim limit, deductible, co-payment, hospital or garage network, waiting period, exclusions, emergency coverage, claim process, and renewal terms.

Related Posts

Insurance for Freelancers in Dubai: Complete Guide

Freelance or self-employed in Dubai? Learn how health, liability, indemnity, and income protection insurance work for expats.

What Happens When Missed Health Insurance Renewal in Dubai?

Missed your health insurance renewal in Dubai? Learn about fines, visa issues, medical bills, grace periods, and what to do next.